Meet the institution that controls the price of money

In the spring of 1907, a man named Charles Barney stood in the lobby of the Knickerbocker Trust Company on the corner of Fifth Avenue and 34th Street in Manhattan. He was its president. He was, by the standards of the Gilded Age, extraordinarily successful. And in about six weeks, he would be dead, by his own hand, in his own home, because the United States of America did not yet have a central bank.

Most Americans think of the Federal Reserve the way we think of the post office, as a thing that is simply there, that has always been there and will always be there, humming in the background. But the Fed is not that old. It was born out of a very specific terror: what happens when an entire nation's financial system depends on the personal whims of one very rich, very old man with a bad temper.

That man, of course, was J.P. Morgan.

J.P. Morgan

For those unfamiliar with the Panic of 1907, here is what you need to know. The Knickerbocker Trust Company, New York City’s 3rd largest trust, made an attempt to corner the market of the United Copper Company. On Tuesday, October 15, 1907, the plan failed spectacularly when the share price of United Copper collapsed. This began a bank run that spread across the nation, causing the 8th largest decline in US Stock market history.

There was no Federal Reserve. There was no deposit insurance. There was no lender of last resort. What there was, instead, was Morgan's library on Madison Avenue, where a 70 year old JP Morgan sat in a red velvet chair, smoking cigars, and decided which banks would live and which would die. He was, for a few harrowing weeks, functioning as a one-man central bank for the most powerful economy on Earth.

Think about that. The entire financial destiny of the United States rested on whether J.P. Morgan felt like answering the door.

And here is the punchline: it worked. Morgan's intervention stopped the panic. The system stabilized. But even Morgan knew the absurdity of the arrangement. "This is the last time," he reportedly told associates. He was right. He died in 1913, the same year Congress enacted the Federal Reserve Act into law.

The lesson the country drew from 1907 was not complicated: we cannot do this again. We cannot leave the fate of the economy to the charity of plutocrats. We need a permanent institution, a lender of last resort, a manager of the money supply, a kind of economic thermostat. What we got was the Federal Reserve System.

Now, before we go any further, I need to tell you what the Fed actually does, because most people, including, I suspect, several members of Congress, have only the vaguest idea.

The Fed conducts monetary policy. This is different from fiscal policy, and the distinction matters enormously, though almost nobody outside of economics departments bothers to make it.

Fiscal policy is what Congress and the President do. It's taxing and spending. It's the decision to build a highway or fund Medicare or send everyone a stimulus check. Fiscal policy is loud. It involves campaigns and debates and speeches. It is, for better or worse, democratic.

Monetary policy is quieter. It is the management of the money supply and interest rates. Higher rates make borrowing more expensive, which slows spending, which (theoretically) cools inflation. Lower rates do the opposite: they make money cheap, encourage borrowing, and stimulate growth.

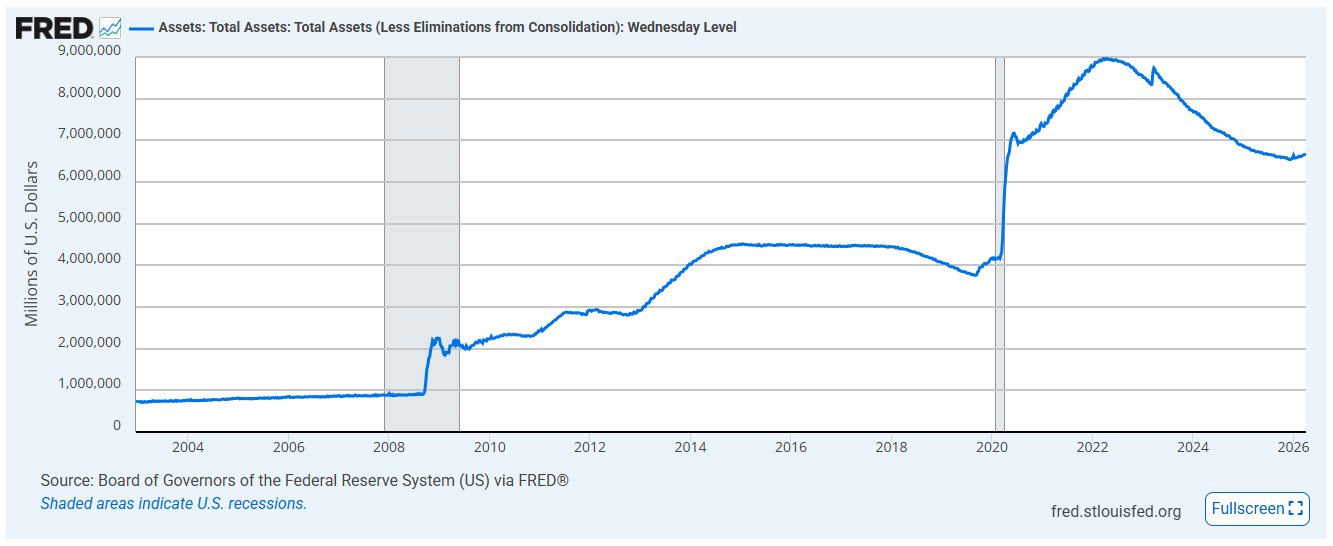

The Fed has a few tools to do this. It can set a benchmark interest rate, the federal funds rate, which is the rate at which banks lend to each other overnight. It can set reserve requirements for bank deposits, restricting or easing the amount of lending banks can do. It can buy or sell government securities on the open market, what's called "open market operations", to increase or decrease the amount of money moving around the banking system. And after 2008, it expanded this power into its now most widely used weapon: quantitative easing, which is essentially the Fed creating money electronically and using it to buy enormous quantities of bonds and mortgage-backed securities. During the financial crisis, the Fed's balance sheet swelled from around $900 billion to over $4.5 trillion.

Total assets of the FED over time

The simplest way to think about it is this: Congress decides where the money goes. The Fed decides how much money there is, and what it costs to borrow it.

But here is where it gets interesting, and, depending on your political persuasion, either reassuring or deeply unsettling.

The Federal Reserve is not part of the federal government. Not exactly. It exists in a kind of constitutional twilight zone, a liminal space that would have made the Founding Fathers profoundly uncomfortable if they could have imagined it.

The Board of Governors is appointed by the President and confirmed by the Senate. So far, so democratic. But once confirmed, those governors serve fourteen-year terms, longer than any president, longer than most senators, and they cannot be removed for policy disagreements. The twelve regional Federal Reserve Banks are technically private institutions, owned by member banks in their districts. The Fed does not receive congressional appropriations. It funds itself from the interest on the securities it holds. It is, in a structural sense, an independent agency that prints its own budget.

This was deliberate. The architects of the Federal Reserve, men like Senator Carter Glass and the economist H. Parker Willis, understood something crucial: monetary policy is too important, and too technical, and too easily corrupted by short-term political incentives, to be left to politicians. A congressman facing re-election in November will always want lower interest rates in October, regardless of what inflation is doing. The whole point of the Fed's independence is to create a buffer between the desire to get re-elected and the need to occasionally do unpopular things, like raising interest rates in order to slow the economy because inflation is running too hot.

William McChesney Martin, who chaired the Fed from 1951 to 1970, once said that the job of the central bank is "to take away the punch bowl just as the party gets going." That is not a job description that wins popularity contests. It is, however, a job description that prevents hangovers.

Let me tell you another story. It's 1979, and the United States is miserable.

Inflation is running at 13 percent. Gas lines stretch around city blocks. The word "stagflation" has entered the vocabulary. The unholy combination of rising prices and economic stagnation that wasn't even supposed to be possible according to the old Keynesian models. Jimmy Carter is in the White House, looking haunted. The country feels as though it is coming apart.

Into this chaos walks Paul Volcker. He is six feet seven inches tall. He smokes cheap cigars. He is not, by any conventional measure, a charming man. And he is about to do something that will cause enormous pain to millions of Americans, crater the housing market, push unemployment above 10 percent, and, this is the important part, save the economy.

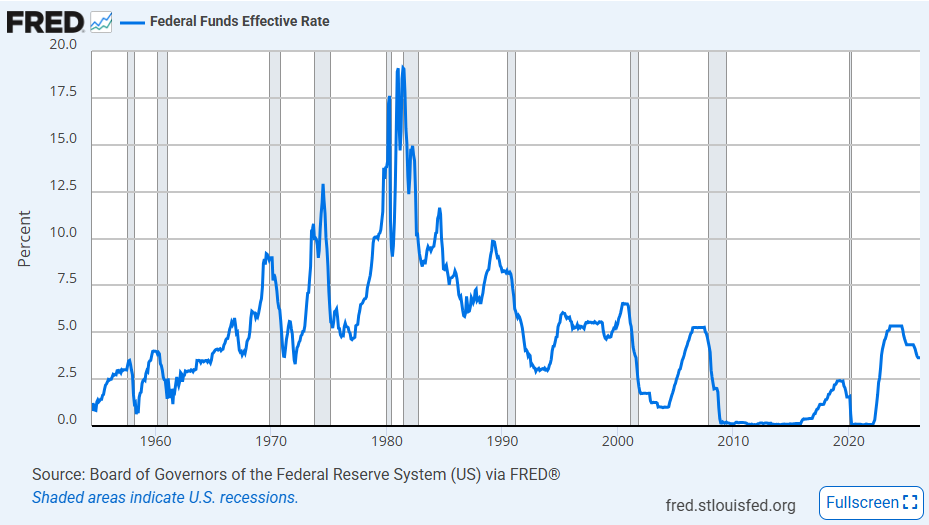

Volcker raised the federal funds rate to 20 percent. Twenty. Let that sink in. If you were buying a house in 1981, your mortgage rate might have been 18 percent. The construction industry collapsed. Farmers went bankrupt. Car dealers couldn't move inventory. Volcker received death threats. Builders mailed him two-by-fours in protest. Members of Congress called for his removal.

But it worked. By 1983, inflation had fallen below 4 percent. The monster was slain. And the long boom of the 1980s and 1990s, the era of declining interest rates, expanding credit, and extraordinary growth, became possible precisely because one unelected official had the institutional independence to inflict short-term pain for long-term gain.

FED effective rate over time

No politician could have done what Volcker did. No president would have survived it. That is the argument for the Fed's peculiar independence. It is the argument that says: some decisions are too important to be popular.

But here is the thing about arguments. They have counter-arguments. And the modern criticisms of the Federal Reserve are not frivolous. They are not the province of cranks and conspiracists. The serious critiques come from both the left and the right, and they converge on a discomforting question: Who watches the watchmen?

Start with the critique from the left. When the financial crisis hit in 2008, the Fed, under Ben Bernanke, moved with breathtaking speed to bail out the banking system. It opened emergency lending facilities. It engineered the sale of Bear Stearns by providing a $29 billion dollar loan and absorbing risky assets. It flooded the system with liquidity. The banks survived. The bankers survived. Many of them, in fact, thrived. Meanwhile, roughly ten million Americans lost their homes. The recovery in employment was agonizingly slow. The recovery in asset prices, stocks, bonds, real estate, was not. Quantitative easing, by design, pushed up the value of financial assets, which are disproportionately held by the wealthy. The Fed did not intend to engineer a massive transfer of wealth upward. But that is, in effect, what happened.

The leftist critique, then, is about distributional consequences. The Fed has a dual mandate: maximum employment and price stability. Lowering interest rates doesn't create jobs directly. It creates conditions in which jobs might be created, eventually, if the right people decide to invest in the right things. In the meantime, it makes rich people richer. "The Fed," as the economist Karen Petrou has argued, operates in a framework that systematically advantages those who already have assets. That is not a conspiracy. It is a structural feature of how monetary policy works.

Now take the critique from the right, which is almost the mirror image. Conservatives argue that the Fed's very existence distorts markets and enables reckless government spending. The argument goes like this: because the Fed can always, in extremis, buy government debt, Congress never faces the true cost of its borrowing. The national debt balloons. The dollar erodes. The boom-bust cycle is not a natural phenomenon, it is a creation of central banking, an artifact of cheap money encouraging speculation and malinvestment that must eventually collapse.

It is not easy to dismiss when you look at the pattern: the dot-com bubble, inflated by easy money in the late 1990s; the housing bubble, fueled by ultra-low rates in the 2000s; the "everything bubble" of the 2020s, arguably stoked by the most aggressive monetary expansion in history. Each crisis is met with lower rates and more liquidity, which plants the seeds of the next crisis. It is, the critics say, a treadmill. And the speed keeps increasing.

Then there is the accountability critique, which transcends left and right. The Fed is, as I mentioned, structurally independent. It audits itself. It sets its own budget. Its deliberations are released with a lag. Its chair testifies before Congress, but Congress has no real power to override its decisions. For an institution that can create trillions of dollars with a keystroke, that level of autonomy is, at minimum, worth questioning.

During the pandemic, the Fed bought corporate bonds for the first time in its history. It effectively put a floor under the junk bond market. It signaled that large corporations could take on enormous risk, because if things went sideways, the central bank would be there. This is what economists call moral hazard, and it is the quiet rot at the center of the modern financial system. If you know you'll be rescued, why bother being careful?

I want to end with a scene. It's December 2023, and Jerome Powell, the current Fed chair, walks to a podium. He announces what the markets have been waiting for: the Fed is signaling rate cuts ahead. The stock market surges. Billions of dollars in wealth are created in minutes. A single sentence from a single man in a single building in Washington has rearranged the financial lives of three hundred million people.

And nobody voted for it.

That is not an indictment. Not exactly. It is a description. The Federal Reserve is one of the most powerful institutions in human history, and it was designed, on purpose, with great care, to be insulated from democratic pressure. Whether that insulation is a feature or a bug depends on which story you find more frightening: the story of 1907, when there was no lender of last resort and the economy dangled from the whims of one old man, or the story of right now, when the lender of last resort answers to almost no one.

The honest answer, I think, is that both stories should keep you up at night. The Fed exists because the alternative was worse. But "better than the alternative" is not the same as "good." It is not the same as "accountable." And it is certainly not the same as "democratic."

J.P. Morgan, playing solitaire in his library, deciding who lives and who dies, we got rid of that. What we replaced it with is more sophisticated, more stable, more resilient. But it is not more transparent. And it is not, in any meaningful sense, ours.

The punch bowl is still there. Someone is still deciding when to take it away. The only question is whether we trust the person holding it.